The Ultimate Guide to Blockchain Implementation

Looking for the ultimate guide to blockchain implementation?

That’s an excellent market with many opportunities to be explored.

How to Implement Blockchain Technology

The most famous use of blockchain technology is cryptocurrency. Indeed, blockchain was actually invented by the now legendary Satoshi Nakamoto to allow for the creation of the world’s first cryptocurrency – bitcoin.

Satoshi came up with the blockchain principle to solve the problem that stood in the way of all digital currencies, namely the “double spending” problem. In all systems up until that point, digital currency could be duplicated, theoretically allowing the same coin to be spent more than once.

By decentralizing the network and instead allowing it to be controlled and maintained by multiple nodes that are not even located in the same geographical area, blockchain finally created a viable way to solve this problem.

Use 1: Integrating Cryptocurrency Transactions

I recently wrote an article for the DevTeamSpace blog detailing the “10 Best Bitcoin Payment Gateways”. In this article, I stressed the advantages of businesses allowing customers to pay in bitcoin and other altcoins.

Any application or website that either sells products, charges membership or subscription fees, accepts donations, or any other kind of payment, can benefit enormously by having a cryptocurrency payment gateway integrated into it.

Adding some form of bitcoin API to your new app will not only help to boost income by drawing in all those people who like to pay in bitcoin but will also help your company to save money as most payment gateway transaction fees are lower than the credit card fees charged by the banks, etc.

Since cryptocurrencies such as the bitcoin network offer anonymous financial transactions, governments and CEOs of all the industries that are threatened by these digital currencies are fond of labeling bitcoin as only being good for drug dealers. This is simply not true.

Many companies including those that offer discreet services such as adult toys, for example, are finding huge benefits in allowing their customers to pay in cryptocurrency.

Hire expert developers for your next project

Since most people often don’t want such transactions to appear on their monthly credit card statements, cryptocurrencies are often viewed as a much-welcomed method of payment.

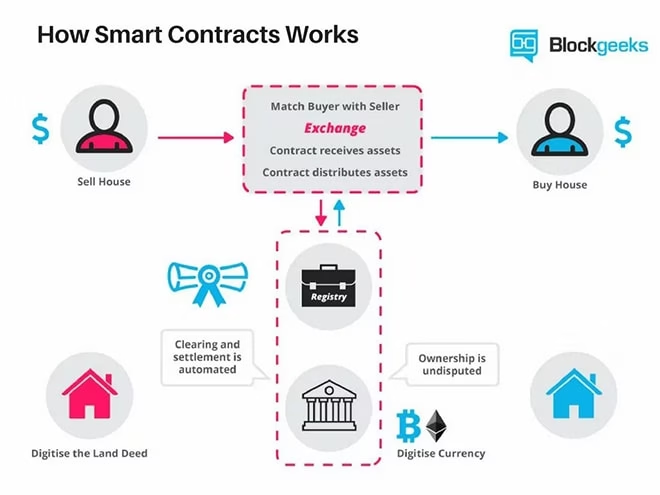

Use 2: Smart Contracts

The use of smart contracts, as championed by such organizations as the Ethereum Project, offers companies access to an enormous range of tools to improve their projects. Smart contracts allow for legally binding agreements to be drawn up between two or more separate parties.

These contracts allow for a much greater level of anonymity and remove the need for a 3rd party, such as a lawyer, for example, to help execute the transaction.

A list of fulfillment criteria can be built into the contract and once these are satisfied, the contract will automatically initiate a set of actions without any need for this to be done manually. Actions could be anything from initiating a payment to validating marriage documents etc.

For more information on the potential uses of smart contracts, read this article.

Smart contracts can be used to facilitate a massive amount of different block transactions. They are set to allow many of the processes that institutions ranging from the finance sector to medical research need to streamline through automation.

It is for this reason that smart contract development is now the focus of many top blockchain developers.

For a more detailed look at how exactly these contacts function and how companies can deploy them, read my article “10 Uses for Smart Contracts”.

Dev teams are racing to develop smart contracts in Solidity, a language that is designed to work with the Ethereum Virtual Machine (EVM), in order to find solutions to specific industry needs.

If you are interested in reading an example of how to write and deploy a smart contract on Ethereum then you can read Hacker Noon’s article on Full-stack smart contract development.

The great thing about smart contracts is that much of the hard work has already been done by the Ethereum Project. This means that even small to medium-sized businesses can begin to implement blockchain-based smart contracts into their projects without needing to employ huge development teams.

Since the Ethereum platform allows smart contracts to be run on its platform there are also no requirements for companies to have to set up a blockchain network either. This means that companies can launch their smart contracts as soon as they are ready.

Use 3: Integrating Smart Devices with IoT

The other really interesting avenue, which many companies are exploring in regards to blockchain integration into their projects at the current time, is securing IoT networks. IoT allows networks of smart devices to be interconnected to help benefit the users from this interconnectivity.

Most of us use IoT already as it is employed for much of the processes that allow our smartphones to control other devices such as our TVs.

Each time you sync your phone with an external speaker you are reaping the benefits of using an IoT network. And this is just the most simple example.

IoT can be used to facilitate complex smart homes, fully automate transactions on supply chains, and one day could even be used to fully automate life inside the spaceships we use for trips to Mars.

In order to give a better picture of how blockchain technology can be implemented into existing/future projects, I am going to look at how blockchain solutions are set to benefit the banking industry.

Case Example: Blockchain Implementation for Banks

Banks are complex institutions that have numerous arms or divisions which allow them to conduct business in numerous areas of finance.

Hire expert developers for your next project

1,200 top developers

us since 2016

Banks are able to offer customer services such as loans, mortgages, etc. while also conducting trade finance and other such activities.

Aside from the much-debated incentives of banks creating their own cryptocurrencies, they stand to gain enormously from implementing blockchain solutions such as smart contracts and blockchain-based IoT networks.

Smart contracts could be employed to help automate many of their key processes. One such example is mortgages. When a customer finds a property they wish to purchase, they could approach the bank, which would then set up a smart contract.

Since the bank already possesses the customer’s entire account history, the first step would include the smart contract establishing their suitability for the required mortgage. Once this has been done, the contract could then initiate a payment to the seller for the property.

This, in turn, would initiate a transfer of the deeds to the buyer and the activation of automatic mortgage repayments from the buyer’s account.

These would continue until the mortgage was fully repaid, at which time the smart contract would deactivate the repayments and end the contract.

The automation of this process could save banks 10’s of millions of dollars every year by reducing the administrative staff needed to process transactions manually. Smart contracts would also lower the risk of mistakes as well as fraud too.

Use 4: Blockchain-based ID protection

In a recent article, ‘How to use blockchain in identity management?‘, I stated that because “globalization increases the need for service integration across domains and geographies, identity management software is becoming more and more important.”

Adding a blockchain-based ID solution will not only help ensure the security of your app but will also reassure customers that they are in safe hands when using your product.

While it might not seem like this is a massive selling point today, the massive surge in data breaches such as the September 2018 Facebook breach where a staggering 50 million user accounts were compromised (leading to some of the first-ever lawsuits where users were given the right to sue the company for better security), is leading to increased awareness regarding the vital need for ID security.

Whether you have the resources to develop your own blockchain-based ID security solution from scratch, or simply decide to integrate an existing blockchain ID solution like Validated ID, offering such a secure solution will certainly help you to stand out from the competition.

Integrating blockchain technology: The key to success lies in planning

Given that blockchain is a niche technology, you surely foresee a complex process when you try to integrate it into your organization, don’t you? You ought to plan such a project meticulously.

Several considerations figure in this planning exercise, e.g.:

- Should you launch a crypto token, or, can you deliver your proposed functionality without one?

- Does a public blockchain network serve your purpose? Well, if you need to limit participants to only trusted parties, then a public blockchain doesn’t work for you. It doesn’t work if you are processing sensitive data and need high scalability either. You should consider using blockchain for an enterprise for such use cases, as I have explained in “Public vs private (permissioned) blockchain comparison”.

- If you are using an enterprise blockchain, are you building one from scratch? That will consume a lot of your time and energy, therefore, I recommend that you use one of the popular enterprise blockchain frameworks. Hyperledger Fabric is a matured framework, moreover, it’s industry-agnostic. You can build a permissioned and scalable blockchain using it where your sensitive data is safe, as our guide “Pros and cons of Hyperledger Fabric for blockchain networks” explains.

- How will you host your blockchain network? Well, you have several options, however, you need to choose the one that works for you. Our guide “What are the Best Blockchain Network Hosts?” could help.

Is this the first time that you are trying to integrate your app with blockchain?

You could use some help with this planning process, and our guide “What to plan for when undertaking blockchain software development?” is just what you need.

Putting together the right blockchain implementation team

The key to successfully implementing blockchain technology into your project is having the right team to do so. Too many managers make the mistake of just offloading projects onto their existing development teams without properly considering the consequences.

As I have already stated, blockchain is a relatively new technology that requires a unique skillset from other types of software development.

Any developer working on blockchain will need to be familiar with such things as cryptography, how a decentralized peer-to-peer network operate, organizations like Ethereum, how they host smart contracts, etc.

It is for this reason that any team should incorporate at least one experienced blockchain developer as well as developers who have the skills and passion to undertake blockchain development.

Hire expert developers for your next project

Any team working with smart contracts should be able to code in Solidity, be familiar with blockchain APIs, and the current platforms offered by blockchain companies to help aid development, etc.

A good blockchain developer will be aware of blockchain platforms such as BigchainDB, which aims to solve blockchain’s scalability problems, Hyperledger, a blockchain platform that allows for the easy creation of a private blockchain, and so on.

Another interesting area is cloud-based blockchain development. Companies such as IBM, Amazon, and Microsoft are now offering blockchain technologies and development spaces on their cloud platforms.

Known as Blockchain as a Service (BaaS), this service is bringing together companies and developers to create viable blockchain solutions for their particular business needs.

The use of platforms such as these can help companies save money as well as help them to get their blockchain projects up and running in much less time.

Projects such as Unibright are now promising companies to bypass developers completely as they don’t require any coding, though the promise that such frameworks offer is still some way off from being able to provide effective solutions for more complex projects.

For this reason, I strongly recommend employing a dev team that is an expert in blockchain deployment. Though costing a little more upfront, often a good development team, that knows how blockchain works, will, in fact, save time and money as the risk of problems is greatly reduced.

Review smart contracts while integrating blockchain technology

I have explained how powerful smart contracts are, however, they pose a key risk. You can’t modify smart contracts after you deploy them. Erroneous smart contracts can adversely impact your operations, and you will find it hard to undo this impact.

Of course, you ought to test them thoroughly. However, as you know, testing blockchain solutions will not unearth all latent bugs. You ought to review smart contracts thoroughly, and this exercise should include the following:

- A static code analysis;

- A code quality analysis;

- Identifying key vulnerabilities like reentrancy, shadowing of variables, overflows, under-flows, incorrect cryptographic signature validation, etc.

- An analysis of whether the smart contracts would deliver their desired functionalities.

Blockchain skills are hard to find, therefore, you might find it even harder to onboard competent smart contracts reviewers! Help is at hand, though! Check out our guide “Undertaking a blockchain code audit and its importance”.

Blockchain Technology Implementation

Though in this very short article I have only been able to touch briefly on this fascinating topic, I hope that it gives you some idea of how to go about integrating blockchain technology into your project.

The simple fact is that most companies have processes that could benefit from the added security and automation that blockchain solutions offer.

It might be a little time before the peg blockchain solutions are commercially available, so the companies that want to get ahead now need to undertake the process of development and implementation themselves.

As I said in the last chapter, companies can smooth out the whole process of blockchain solution implementation by making sure that they have the best possible development team working for them. After all, developers remain an essential key to your project’s success.

Read our guide “How to find a good software developer” for more information.

If you are still looking for experienced software developers to help you with blockchain implementation, DevTeam.Space can help you. Write to us your initial specification for blockchain implementations via this link and partner with our field-expert blockchain developer community.

Frequently Asked Questions on blockchain implementation

It is the use or substitution of blockchain solutions into existing processes or software systems. It involves creating new software such as blockchain applications that are then used to allow traditional processes to be upgraded.

The answer to this question really depends on how complex the solution is required to be. Implementing a simple blockchain solution such as a cryptocurrency token system is relatively straightforward for example. A more complex solution such as one that automates supply chains using smart contracts and blockchain protocol is more difficult.

Some of the best blockchain experts are to be found in DevTeam.Space community. Simply submit a project specification form and a dedicated account manager will contact you to answer all your questions.

Alexey Semeney

Founder of DevTeam.Space

Hire Alexey and His Team

To Build a Great Product

Alexey is the founder of DevTeam.Space. He is award nominee among TOP 26 mentors of FI's 'Global Startup Mentor Awards'.

Hire Expert Developers